The Real Cost of NSA Arbitration

An In-Depth Review of More Than 1.25 Million Federal Disputes

Moving To Self-Funded Health Plan Guide

February 2, 2022

Over half the United States’ non-elderly population — some 150 million people — receive health benefits coverage through an employer-based healthcare plan. Of that 150 million, about 92 million individuals are covered by self-funded or partially self-funded healthcare plans, yet many people remain unfamiliar with the term.

With such a substantial group already participating in self-funded health plans, it’s important to understand its principles as well as how self-funding may provide unique cost-containment opportunities within the landscape of today’s rising premium and healthcare costs. We will explore the advantages self-funded health coverage provides over “traditional” fully insured plans — and whether everyone can make the transition.

What Is a Self-Funded Health Plan?

Both fully insured and self-funded health plans operate under the same basic principle. Money is collected and used to pay for medical expenses of the insured population, with the extent and terms of that coverage being outlined and detailed in a policy or plan document. The more people there are contributing to this fund (the risk pool), the fund is better able to bear an occasional “high dollar” or catastrophic expense.

Fully insured health plans accept a fixed payment (premium) to assume financial risk for medical expenses (the applicable insurance carrier pays the medical bills with its own assets, so if the premium collected exceeds the claims paid – the carrier keeps the balance; if the claims paid exceed the premium collected, the carrier suffers the loss). Self-funded plans, however, do not pass that responsibility onto a third party. In this model, a company’s self-funded plan pays claims with the plan sponsor’s own assets (the plan sponsor is usually the employer and employees, contributing to the plan). These payments occur in a manner which mirrors insurance only from the participants’ perspective, pulling from an established medical trust built up from participating employees’ contributions and/or direct company funds, however – if the claims paid are less than the contributions collected, the employer and employees keep the surplus, rather than lose those funds to a carrier.

Let’s break down this comparison further.

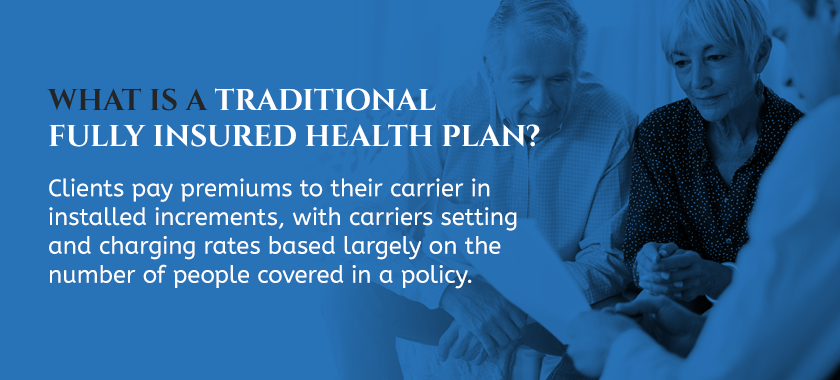

What Is a Traditional Fully Insured Health Plan?

Most people assume they have traditional, fully insured health insurance. They assume this for two reasons. First, almost everyone has a direct relationship with full insurance, in the form of auto insurance, homeowner’s insurance, renter’s insurance, etc. In other words, individual people who purchase insurance do so through a fully insured model. Only in health benefits is self-funding so popular. This is because employers provide health benefits coverage in a group setting. Sadly, this means the individual employees (the plan participants) are not aware of how their health benefits are funded; only that their employer set it up. As such, they assume that their health insurance is funded the same way as their home and car. Next, most self-funded plans use a network (a PPO, HMO, etc.), and these networks are rented from large well-known insurance carriers (such as Blue Cross, Aetna, United, and Cigna). As a result, these carriers’ logos appear on plan documents and health plan ID cards, leading people to assume they have “insurance” with that carrier – not just access to their network.

As discussed, however, being self-funded is very different, despite having access to the same network. Fully insured health plans revolve around fixed premiums. Enrollees pay premiums to their carrier in installed increments, with carriers setting and charging rates based largely on the number of people covered in a policy and their expected claim expense. Traditionally, much of the cost for this entire healthcare package, including the carrier’s profit margin and operating expenses, has been passed along to the individual employees, who have little say in prices and coverage.

In turn, the carrier manages claims and administers the coverage but pockets any money left over from the year, i.e., premiums minus actual claims paid. In order to tilt the scale in their favor, carriers calculate fully insured plans’ premiums using the following:

- Claims Projections: The monetary sum of healthcare reimbursements the carrier expects to issue to the insureds in one year.

- Pooling Charges: To reduce volatility and liability for the carriers as they take on greater and greater policy-holder risks and larger groups of covered persons.

- Administrative Fees: Claims processing, medical management, facility and prescription network usage— the administrative work that underlies the healthcare industry is built into premiums.

- Taxes: Each state has specific health insurance regulations, compliance requirements and medical policies it must adhere to. Taxes can also apply to insurance premiums, which carriers account for and add onto final rates.

- Carrier’s Profit: Carriers must turn a profit if they want to stay in business. They build profit margins into premiums to help ensure this business objective is met.

Based on this model, it benefits health insurance carriers to raise premiums regardless of the year’s actual claim amounts and their own expenses, since they pocket any difference as pure profit. If eligible claims are low for that year, their profit margin is high — but employers and employees don’t get any sort of “refund” and might still see rate hikes the following year.

How Is Self-Funded Health Insurance Different?

Self-funded health benefit plans still pay claims and still have incremental payments to deal with as well — only now, they are handled by the insured entity (the employer) and not a third party (a carrier). As an employer, you would collect contributions, store them in an interest-earning reserve, hire a third-party administrator (TPA) to pay claims using your own assets, as well as create and revise the plan to meet your population’s specific needs. With a self-funded plan, you would be able to exercise more discretion in designing your plan and selecting the coverage and networks most ideal for your workforce. You get:

- No pooling risk. Self-funded policies are covered under the federal Employee Retirement Income Security Act (ERISA) and do not need to account for the same kind of pooling volatility, since their “risk” pool is limited to their own enrolled participants. Your plan will not have to pay more to absorb the risk of other, more costly plans.

- No profit margin: Even more advantageous, there is no carrier making a profit off your premium payments. You get to utilize any money left over to reduce contribution rates going forward or increase coverage.

- Lower administrative fees: Self-funded plans will still pay for claims processing, stop-loss insurance coverage and network contract drafting, either done in-house or through the assistance of a third-party administrator (TPA). These administrative fees tend to be lower than their fully insured counterparts, though.

Top Reasons Employers Make the Switch to Self-Funding Health Plans

Nearly all the major health insurers in the United States now offer some form of self-funded healthcare coverage, either through an administrative services only (“ASO”) contract, or, through a TPA they own. Additionally, there are many independent TPAs to choose from as well. While self-funding is already a very large share of health coverage offerings nationwide, it is still growing, and major carriers (which in the past competed with self-funding and offered a self-funded option as a formality) are now jumping into the game and investing many more resources toward their self-funded business. It is indicative of the fact that this market is already huge and growing. Here are a few reasons we’ve seen companies making the switch:

1. Pay Out Claims as They Occur

One of the biggest advantages of self-funded health plans is their “pay-as-you-go” claims nature. Rather than paying out large coverage payments or setting up expensive premium installments, companies that self fund simply make claims reimbursements on an as-needed basis. Claims costs vary month-to-month and are principally affected only by the care utilized by covered persons, not hypotheticals and projections.

2. Pick the Most Beneficial Plan and Network

Companies that adopt a self-funded plan customize it to their employees’ exact needs. What’s more, claims can be monitored directly using claims analysis software, with coverage adjustments made the following year to better meet your employees’ data-backed healthcare needs.

3. Gain More Savings as a Benefit

If claims are lower than anticipated for the month, your plan and your participants benefit, not a carrier. You can even earn interest on healthcare reserves when stored in the right account type, further incentivizing money saved.

Key Points to Consider When Making the Switch

Transitioning from a fully insured health plan to a self-funded one takes time and commitment. The switch also involves risk.

1. Shock Claims

Shock claims are those “catastrophic” claims that are so large, they essentially drain the self-funding reserves that were meant to cover your entire employee pool for the year. Since the innate advantage and core goal of self-funding is to avoid excessive payments, mainly in the form of high premiums, (subsequently freeing up cash flows), shock claims could potentially derail the entire model. It is the largest risk to this form of healthcare coverage, but there are industry solutions in place to reduce this risk.

There are two main solutions addressing shock claims:

- Individual Stop Loss (ISL): ISL protects against large claims incurred by individuals by creating a payment threshold or “specific deductible.” If any single claim goes over that determined threshold amount, ISL kicks in to reimburse the plan for claims subsequently paid beyond that deductible amount.

- Aggregate Stop Loss (ASL): ASL provides the same protection as ISL, only for an aggregation of smaller claims that add up to a total threshold amount rather than a handful of extreme ones. Aggregate stop loss kicks in once the total number of claims hits the predetermined benchmark, after which claims paid by the plan more than that threshold are reimbursed to the plan.

2. People Covered

How viable self-funded healthcare is for your company depends on a great many factors. These include (but are by no means limited to) the size of your participant population (depth of the risk pool), the demographic makeup of your workforce, and the healthcare market in which you operate.

Stop-loss “reinsurance” carriers are working hard to make self-funding viable for a broader group of employers. Innovative new programs are being developed to expand self-funded plans into smaller organizations and markets. Using models that prioritize an individual business’s financial discipline, its employees’ health and its overall risk tolerance alongside ISL and ASL coverage, plans can be drawn to fit businesses and institutions with increasingly smaller risk pools, allowing smaller and smaller companies to benefit from this model.

Fiduciary Issues for Self-Funded Plans

Under the Employee Retirement Income Security Act of 1974 (“ERISA”), private self-funded benefit plans are exempt from State insurance laws. In other words, these plans must comply with Federal law but can avoid compliance with many burdensome State based laws. Yet, along with these benefits, ERISA also imposes some extra duties as well. Companies with self-funded health plans must appoint individuals with discretionary authority over the plan and its assets. These appointees must be named in the plan document and are responsible for overseeing and managing the institution’s self-funding policies.

These appointed individuals qualify as fiduciaries and must adhere to the following responsibilities:

- Providing benefits for and acting in the best interest of plan participants (i.e., covered persons).

- Following the tenets and provisions of the company’s self-funded plan, as outlined in its core plan documents.

- Holding and monitoring the plan’s assets in appropriate reserve funds.

- Paying sound and reasonable plan expenses.

- Following general fiduciary codes and standards of conduct.

It’s important to note employers can appoint in-house fiduciaries as well as hire outside fiduciary counsel, often in the form of a third-party administrator (assuming the TPA is willing to do so).

Tax Considerations for Self-Funded Plans

Self-funded and fully insured plans fall into overlapping tax considerations and applicability. Of those similarities, employee contributions, company contributions and claims paid are each considered tax-free, however, tax and legal implications for self-funding organizations still remain, while others are avoided.

1. State Premium Taxes

Unlike traditional fully insured coverage, self-funded programs do not pay state premium taxes. These taxes average between 2 and 3 percent of the premium’s dollar value. Most carriers include that tax percentage in annual premium quotes, with many employees unaware they’re paying them.

2. State-Mandated Benefits and Fees

In addition to avoiding premium taxes, self-funded plans are also exempt from most state insurance laws. Because organizations customize their coverage, this also means an exemption from associated fees and compliance audits, for example, the Health Insurance Marketplace User Fee. Exemptions from state-mandated benefits tend to reduce both the costs and complexity of providing coverage, benefiting businesses that go this route.

3. Internal Revenue Codes (IRC)

More commonly known as the IRS Tax Codes, the IRC includes taxation parameters on healthcare coverage programs. Self-funded plans must adhere to IRC §§104, 105, 106, 162, 213, 4976 and 5000, plus they can face tax consequences if found to be operating discriminatory coverage tactics under IRC § 105(h).

4. Death Benefits and Taxes

Death benefits are taxed differently under self-funded healthcare plans. More specifically, IRC § 101 (b) does not apply to self-funded plans, meaning an employee’s death benefit that transfers to beneficiaries may qualify under a different tax rate.

Compliance Considerations for Fully Insured vs. Self-Funded Plans

Self-funded health plans must comply with all of the following laws:

- Health Insurance Portability and Accountability Act (HIPAA)

- Employee Retirement Income Security Act (ERISA)

- Americans with Disabilities Act (ADA)

- Pregnancy Discrimination Act

- Age Discrimination in Employment Act

- Economic Recovery Tax Act (ERTA)

- Tax Equity and Fiscal Responsibility Act (TEFRA)

- Deficit Reduction Act (DEFRA)

- Consolidated Omnibus Budget Reconciliation Act (COBRA)

Compliance is again at the federal, not state-audited, level and is overseen by an in-house employee, a TPA or legal counsel – functioning as the plan administrator and fiduciary. Please note this is not an exhaustive list.

Documentation for Fully Insured Vs. Self-Funded Plans

In addition, proper documentation for a self-funded health plan is relatively straightforward. Core documents for a compliant program will include:

- Plan Documents: A formal document or set of written documents outlining the entire self-funded plan must be drafted and maintained by an in-house appointee and/or a self-funded health plan consultant TPA. Often, a self-funded plan will simply utilize a well written Summary Plan Description (SPD) as its plan document, thereby reducing the plan to one document.

- Summary of Benefits and Coverage (SBC) and Summary Plan Description (SPD): A summary of employee coverage and health benefits must be written in clear and easy-to-understand language, including a glossary of terms and network information. These are included in the SPD given to covered persons detailing their plan rights and individual obligations alongside a certificate of insurance.

- Stop-Loss Policies: These are needed if purchasing these through a stop-loss provider.

- Form 5500: As part of federal-governing ERISA reporting requirements, organizations that are self-funding do not have to file a Schedule A under ERISA annual reports, but they do have other filing requirements.

- Affordable Care Act (ACA) Reporting and Tax Returns: Self-funded plans file the ACA’s 1094-B and 1095-B series in order to remain compliant, as well as file for tax-exemptions under VEBA status.

Self-Funded Plan Transitions

Switching from a fully insured policy to a self-funded plan takes some time, on average two years of preparation and set-up. Organizations fully committed to and with the resources in place to execute all transition steps can cut that lead time down to six to 12 months. Conduct a self-funded health plan evaluation to ensure you have addressed the following:

- Create an Action Plan: Outline your timeline, as well as contact all vested parties to begin drafting planning documents and core policies.

- Coordinate and Contract Involved Parties to Draft the Plan Document: At the very least, this will include a third-party administrator or other party contracted to help draft the plan documents and formal SBC and SPD, plus any partner fiduciaries, certified public accountants and account brokers necessary to see these documents come to fruition from a compliance standpoint.

- Finalize Plan Policies and Coverage: Ensuring ERISA, HIPAA and other regulatory mandates are met and standards of conduct under the new plan remain in full compliance with federal laws.

- Acquire Stop-Loss Policies: For risk-mitigation and to ensure your organization is protected in the event of shock claims.

- Draft Administrative Service Agreements: Appointing and outlining the duties of an in-house plan administrator or a contract with a TPA.

- Publish SBCs and SPDs: For all employees and covered persons.

- Consider ERISA Bonds and Fiduciary Liability Insurance: All as a final risk mitigation strategy, protecting your assets and reputation in the event of policy mishandlings, fraudulent activity or breaches of federal laws by any of your appointed administrative agents is crucial.

Contact The Phia Group, LLC, for Self-Funded Health Plan Consulting

We understand this transition can be complex, with new risks and rewards to balance. The Phia Group has been on a mission to make health benefits more affordable for employees and employers alike since our inception, with cost-containment services tailored to our clients.

Get in touch with one of our self-funding health insurance consultants today. We can discuss if a self-funded plan transition suits your organization. Let us help you maximize benefits while minimizing costs so you can take back control of your operations.