The Real Cost of NSA Arbitration

An In-Depth Review of More Than 1.25 Million Federal Disputes

The No Surprises Act Explained

July 11, 2022

The No Surprises Act was passed to protect patients from unexpected medical bills from out-of-network providers. The details of the Act can be confusing, so we’re here to explain whom it affects, how it will impact costs, and other details.

What Is the No Surprises Act?

Lawmakers signed the No Surprises Act into law at the end of 2020 as part of the Omnibus Appropriations Bill. It protects patients from having to pay what have been dubbed “surprise bills” from out-of-network providers.

Here’s an example of how the No Surprises Act will impact patients. Let’s say you go to the hospital for what you think is heartburn, but you end up having emergency surgery for complications related to a heart attack. Before this Act, if there were no cardiologists at the hospital who were in-network for you when you needed life-saving surgery, you may have been on the hook for any out-of-pocket costs associated with the out-of-network treatment you received. Imagine having to deal with the news that you’ve just had a heart attack while trying to figure out how you’re going to pay off a bill you didn’t expect. This Act is designed to protect you from unexpected bills like these.

What Medical Services Will Be Affected

The No Surprises Act applies to several classes of out-of-network or otherwise non-contracted medical services, including:

- Air ambulance services

- Emergency services (except for ground ambulances)

- Services provided to stabilize a patient post-trauma

- Out-of-network services at an in-network facility if the provider didn’t notify the patient that the services were out-of-network and obtain patient approval of the same

Whom Does the No Surprises Act Affect?

This Act primarily impacts consumers who need emergency medical care or patients who otherwise do not get a say in being treated by an out-of-network provider. The No Surprises Act may affect some consumers more than others, including parents and indigent patients.

In general, the No Surprises Act will apply to almost all private healthcare plans and non-group health insurance policies. This means the new law will protect most consumers with private healthcare, such as an employer-sponsored group plan, and consumers with non-group health insurance policies from surprise costs. Consumers with health insurance no longer have to worry about paying more than in-network prices for out-of-network emergency services or services from an out-of-network doctor in an in-network medical facility.

This particular feature of the No Surprises Act is especially critical for low-income consumers. Low-income patients sometimes avoid inconvenient medical care even if they have some form of insurance, which can increase the number and cost of emergency services they need down the line. The Act helps protect low-income consumers from being forced to choose between feeding their families and paying an out-of-network emergency medical fee to protect their credit.

If a consumer schedules an appointment with an out-of-network provider who works at an in-network facility, the facility must provide the consumer with a written notice that includes possible charges the consumer might receive if they decide to keep the appointment. The facility must also provide the patient with a list of in-network doctors that could provide the same services the consumer wants. These written notices must be given to the consumer at least 72 hours before the provider has scheduled the consumer for an appointment. The consumer must then sign the notice and return it to the facility before they receive care.

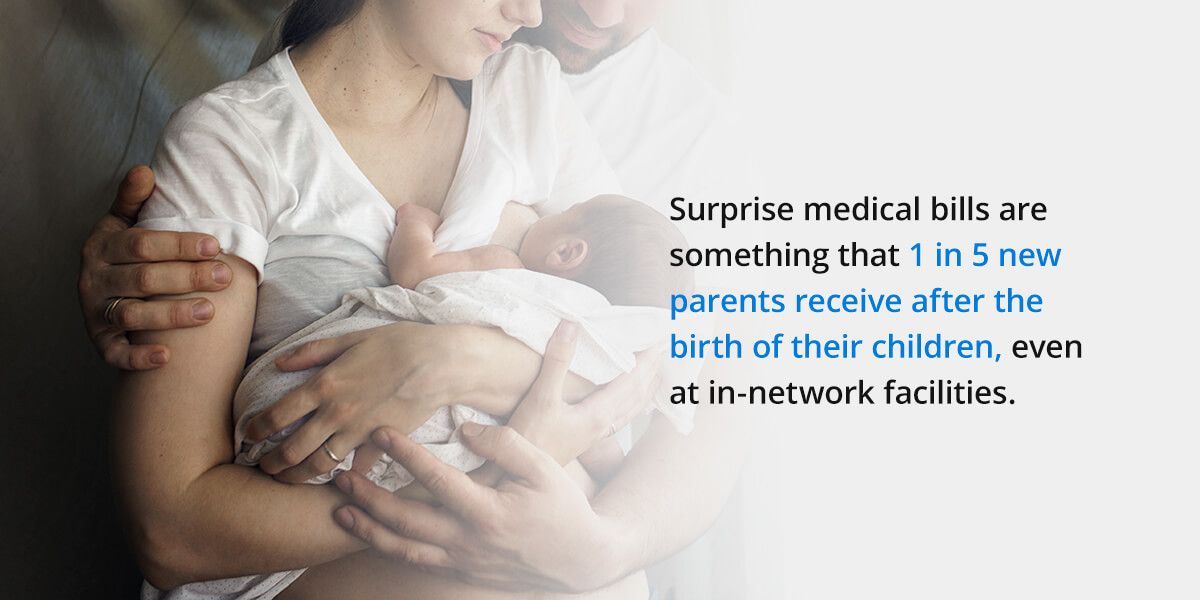

1 in 5 new parents receive surprise medical bills after the birth of their children, even at in-network facilities. Around one-third of parents end up with surprise medical bills that are more than $2,000. Even if the births are pre-planned, parents risk having to pay more than expected. Preparing and planning for a baby is costly enough already, without surprise bills to worry about.

Medical services that typically cause new parents to receive surprise bills include cesarean sections, anesthesia, and intensive neonatal care. The NSA’s new protections can be a weight off new parents’ shoulders.

How Will the No Surprises Act Impact Healthcare Costs?

Lawmakers passed the No Surprises Act to protect consumers from surprise medical bills, but many people wonder if it will also lower healthcare costs for consumers.

Under this new law, providers cannot easily increase prices for certain medical bills, whereas prior to the Act’s passage, medical billing went wholly unchecked. It stands to reason that contracts with providers would also ultimately be more favorable to payors, which can in turn lead to lower healthcare costs for health plans, and therefore lower costs for insureds.

The Congressional Budget Office predicted three instances of how the No Surprises Act may affect healthcare costs:

- The Act will save consumers around $34 billion due to cost-sharing and lower premiums.

- The Act will cause a 0.5% to 1% decrease in commercial insurance premiums.

- The Act will save taxpayers $17 billion over the next 10 years.

Additional Considerations with the No Surprises Act

In addition to affecting patients with out-of-network bills, the No Surprises Act also covers arbitration and initial payments to providers.

Arbitration

If an out-of-network provider is unhappy with how much they are allowed to bill a patient for medical services, they can initiate an arbitration process described in the No Surprises Act. An arbitrator will consider both the payment amount the provider feels is fair and the payment amount the insurer thinks is fair. The arbitrator will then decide which amount the insurer will pay. There is no middle ground; the arbitrator must choose one of the two submitted amounts, resulting in one winner and one loser.

Provider groups demanded this arbitration process to allow out-of-network providers to avoid a pattern of being paid nothing or very little for expensive medical procedures. This process seems to lean towards benefitting providers over consumers since arbitrators must consider the following provider-friendly factors when making their decision:

- The average rates for medical services in the area where the out-of-network provider works and other economic factors relating to that area

- The rates of previous contracts between the provider and the insurer

- The level of training the provider in question has undergone

- The market shares of the health plan and the out-of-network provider

- Believable efforts of provider and insurer to reach a settlement

Professionals have estimated that it may take one to two months and possibly longer for providers to receive payment after initiating the arbitration process, leading to discourse that the time delay may deter providers from utilizing the arbitration process in many cases. Additionally, if a provider wants to initiate another arbitration process with the same insurer concerning similar services, they have to wait 90 days to do so.

The federal government will oversee the creation of a process to detect and eliminate any conflicts of interest that the arbitrator might have, while also ensuring that the arbitrator has the necessary skills to take part in the arbitration process, which adds even more to the federal government’s plate when it comes to preparing for this new act.

This new law encourages settlements in place of the arbitration process by requiring all arbitration cases to be recorded for public use. This public record will allow the parties in potential future arbitrations to be able to get a better idea of whether it would be worth it for them to go through with the arbitration, or if settlement would be a better option for either party.

Initial Payment

The No Surprises Act requires health insurers to pay out-of-network providers within 30 days of the service they provide to a patient. However, the Act does not specify the amount the insurer must pay the provider. There are certain provisions regarding how patient cost-sharing must be calculated and what happens in the event the provider disputes the initial payment as unreasonably low, but no explicit provision of the No Surprises Act actually requires a particular amount of payment.

Contact Us About Our Patient Defender Offering

One of our goals at The Phia Group is to protect patients, much like the No Surprises Act intends to do. Business owners often experience issues with employees being balance- billed, especially after employees receive unexpected or emergent medical care. With our out-of-network solutions, we can help avoid these payment disputes to begin with – and in the case of disputes, balance billing, or collection efforts, you and your employees will never have to navigate these tricky processes alone.

If you need assistance complying with or understanding the No Surprises Act, or if employees experience balance billing and collections, our various claim management services can help provide your employees with a professional advocate, in an effort to minimize disruption and keep your healthcare plan costs consistent.

If you would like to learn more information about the No Surprises Act, listen to our webinar.

Contact us online or at 888-986-0080 to learn more about our claim management services.